Interest rates are rising, but we're not alone

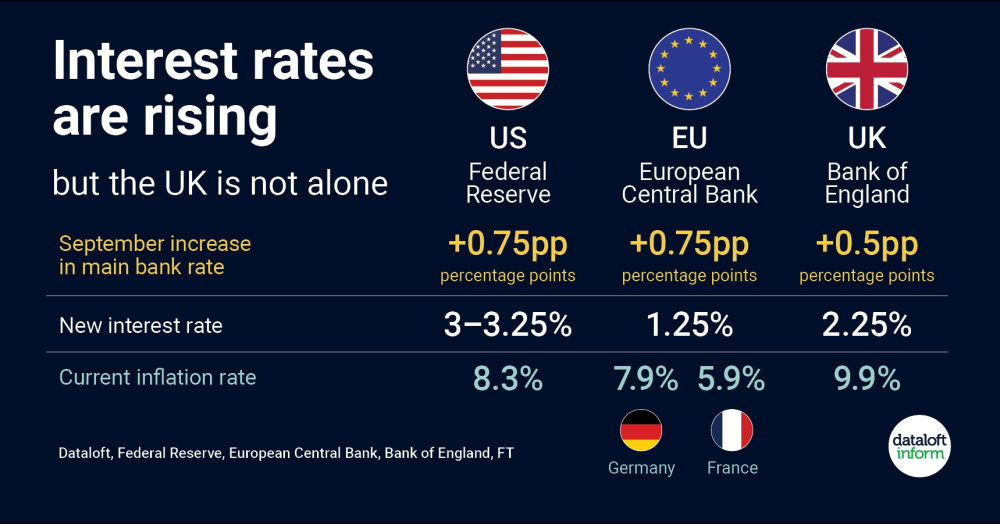

In the September meeting, the Bank of England increased its bank rate to 2.25%. Its seventh consecutive rise and again increasing the rate by a significant amount (+0.5 percentage points).

Many UK borrowers are protected from any immediate increase by fixed rates (representing 94% of new mortgages*) but borrowing costs are rising for many existing and all new borrowers.

The Bank of England needed to take decisive action to ensure high inflation doesn’t become entrenched. The UK is certainly not alone in this; the Federal Reserve in the US also increased rates significantly this month, so too the

European Central Bank.

Consensus forecasts, compiled by HM Treasury, suggest that UK inflation could be back to more normal levels for 2023 at 4.5%. Source: Dataloft, Financial Conduct Authority, Q1 2022 data, Federal Reserve, European Central Bank, Bank of England, FT